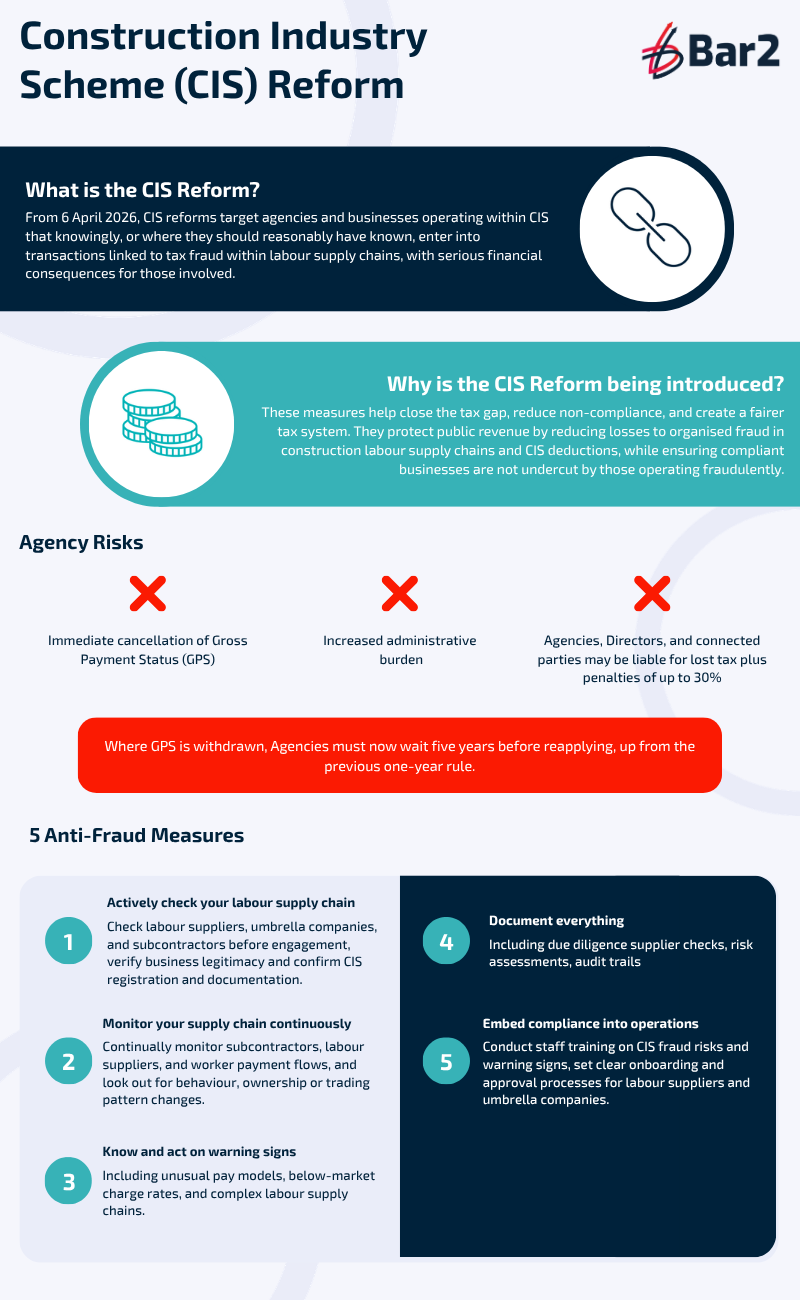

From 6 April 2026, major changes to CIS reshaped how labour supply chains are regulated in the UK. These reforms clamp down on tax fraud, tighten compliance responsibilities for agencies, and ensure workers are taxed correctly based on how they actually operate.

CIS Reform 2026 - What's changed?

The CIS reform introduces new compliance expectations for agencies and businesses operating within the construction labour supply chain. From April 2026, these measures target organisations that knowingly, or where they should reasonably have known, enter into transactions linked to tax fraud involving labour supply.

Where non-compliance is identified, the financial consequences can be significant.

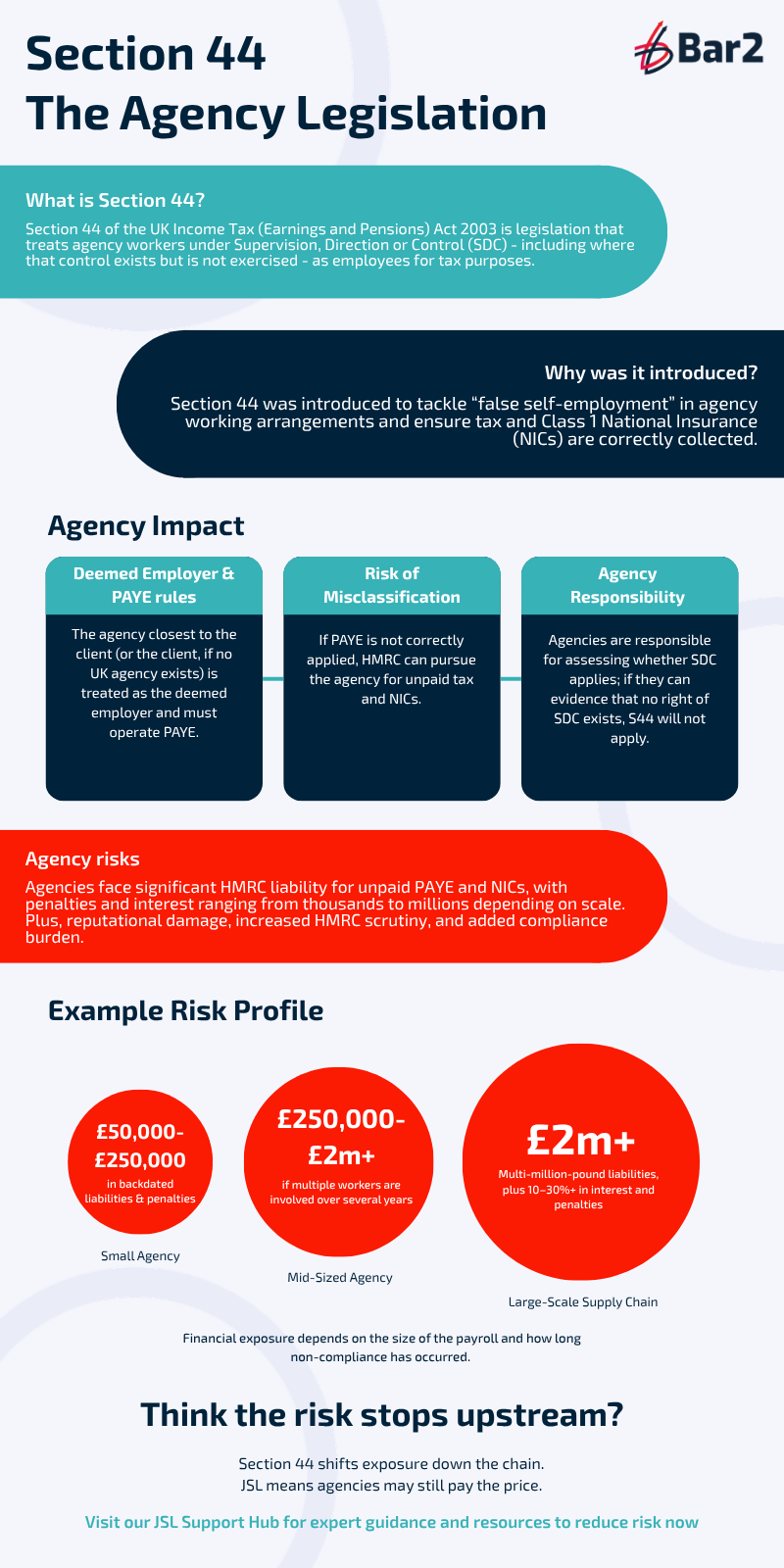

What is Section 44 of the Agency Legislation?

Section 44 of the Income Tax (Earnings and Pensions) Act 2003 is a UK tax legislation that impacts agency workers. It applies where workers are engaged under conditions of Supervision, Direction or Control (SDC), including situations where such control exists, even if it is not actively exercised.

When Section 44 applies, the worker is treated as an employee for tax purposes, meaning PAYE and Class 1 National Insurance Contributions (NICs) must be correctly operated.

Together, these reforms reinforce a fairer, more transparent labour market with stronger enforcement against non-compliance.

Understanding S44 and Supervision, Direction & Control (SDC)

One chain, shared responsibility

With CIS Reform and Section 44 strengthening Joint & Several Liability (JSL), compliance and tax risks are no longer confined to a single business in the chain.

Learn 5 ways to protect your business in our JSL Support Hub:

The Friday Payroll Club

Join us every last Friday of the month as we break down payroll, compliance, and industry trends — without the fluff!